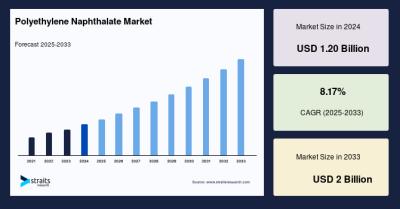

The global polyethylene naphthalate market size was valued at USD 1.20 billion in 2024 and is projected to reach from USD 1.27 billion in 2025 to USD 2 billion by 2033, growing at a CAGR of 8.17% during the forecast period (2025-2033). The growth of the market is attributed to the rising demand in beverage bottling.

Polyethylene naphthalate is a high-performance polyester known for greater thermal and mechanical resilience compared to PET. Its outstanding barrier qualities effectively extend the shelf life of packaged food and beverages by protecting against oxygen and carbon dioxide ingress. Additionally, PEN withstands higher sterilization temperatures, enabling its use in hot-fill applications such as teas and dairy drinks. These attributes have fueled its expanding adoption in beverage bottling, packaging, and pharmaceutical sectors, where product freshness and safety are paramount.

Beyond packaging, PEN’s excellent thermal and dielectric properties have made it an essential material in advanced electronics. It is widely used in flexible printed circuits, foldable displays, battery separators, and insulation films. The automotive sector benefits from PEN’s mechanical strength and thermal resistance for applications like lightweight components, sensors, and electric vehicle battery insulation. PEN films also increasingly feature in renewable energy technologies, including photovoltaic solar panels, due to their durability and environmental resistance.

The packaging segment continues to dominate the PEN market, owing to the material’s ability to produce lightweight, durable packaging that preserves product quality without heavy reliance on preservatives. Beverage bottling leads this application category, with a notable upswing in demand for PEN-based bottles that enhance product shelf life and sustainability. Major beverage companies have incorporated PEN blends to meet evolving consumer preferences for premium, eco-friendlier packaging.

Electronics and automotive applications constitute other significant market segments. PEN’s superior dimensional accuracy, electrical insulation, and thermal stability make it ideal for increasingly miniaturized and flexible electronic components. Similarly, the automotive industry’s shift toward fuel-efficient, lightweight vehicles underpins rising PEN use in high-performance tires and electronic sensors.

Asia-Pacific commands the largest share of the polyethylene naphthalate market, accounting for around 60.6% of global revenue as of 2024. The region’s dominance stems from its expansive manufacturing base, thriving electronics and automotive sectors, and growing consumer markets for packaged goods. Countries like China, Japan, South Korea, and India are key contributors, leveraging PEN in applications ranging from OLED displays and flexible electronics to premium beverage packaging. Government policies promoting sustainability and circular economy initiatives further bolster PEN adoption in these markets.

North America represents the fastest-growing region, propelled by heightened consumer demand for sustainable packaging, advancements in electronics manufacturing, and expansion of the electric vehicle market. The United States leads regional growth, with beverage giants utilizing PEN to improve recyclability and shelf life of products. Canada also contributes through growing environmental awareness and investments in clean technologies.

Europe holds a significant market position as well, driven by stringent sustainability regulations, the automotive industry’s demand for lightweight high-performance materials, and expanding use of PEN in food and beverage packaging. Countries like Germany, the UK, and France are pioneering innovations in PEN applications aligned with EU Green Deal directives and extended producer responsibility laws.

Despite its advantages, PEN’s higher production costs remain a barrier to wider market penetration. The complex polymerization process and costly raw materials such as naphthalene dicarboxylic acid increase manufacturing expenses compared to alternatives like PET. This cost factor limits PEN’s adoption in price-sensitive sectors and emerging markets where affordability is critical.

Furthermore, PEN recycling infrastructure is not as mature as PET’s, posing end-of-life management challenges. These factors create hesitancy among some manufacturers to fully transition to PEN-based systems. However, ongoing research efforts aim to reduce production costs and enhance sustainability. Industry leaders are exploring bio-based PEN variants and advanced recycling technologies. For instance, pilot programs deploying recycled feedstock to produce PEN films are underway, expected to improve competitiveness and environmental appeal in the near future.

The polyethylene naphthalate market is characterized by intense competition among key players focusing on innovation, sustainability, and regional expansion. Companies like Teijin Limited dominate the market with significant production capacity and substantial R&D investment in high-performance PEN applications. Others are expanding distribution networks across emerging economies and developing specialty PEN grades tailored to specific end-use requirements.

The polyethylene naphthalate market outlook is positive, underpinned by increasing demand for sustainable, high-performance materials in diverse applications. The packaging and beverage industries will continue to drive volume growth, especially in regions with rising disposable incomes and environmental awareness. Advances in electronics, automotive, and renewable energy sectors will further augment PEN adoption. With cost and recycling challenges gradually addressed through innovation, PEN is likely to solidify its position as a material of choice for next-generation packaging and advanced industrial applications.