Industrial floor coatings are specialized protective layers applied to floors in industrial settings such as factories, warehouses, and commercial facilities. These coatings are designed to enhance durability, resist wear and chemical exposure, and improve safety by providing anti-slip properties on surfaces that endure heavy machinery, high traffic, and harsh environmental conditions. The market for industrial floor coatings has witnessed significant growth, and this trend is set to continue as industries increasingly prioritize floor protection, safety, and operational efficiency.

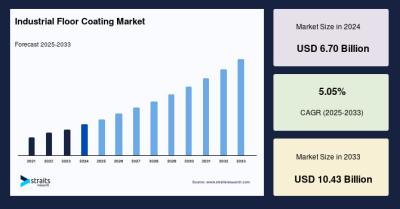

The global industrial floor coating market size was valued at USD 6.70 billion in 2024 and is projected to grow from USD 7.03 billion in 2025 to reach USD 10.43 billion by 2033, growing at a CAGR of 5.05% during the forecast period (2025–2033).

The booming construction industry, particularly within commercial and industrial infrastructure, continues to fuel demand for advanced floor coatings that contribute to durable and safe working environments.

Several factors are propelling the industrial floor coating market forward. First, the rapid development of manufacturing facilities and industrial zones necessitates robust floor solutions that withstand mechanical abrasion, chemical spills, and heavy traffic. Second, there is a growing emphasis on workplace safety and cleanliness, which has increased adoption of coatings with anti-slip and antimicrobial properties. These coatings are especially important in industries with strict hygiene standards, such as pharmaceuticals, food processing, and healthcare.

Technological innovations also play a crucial role. Advanced coating technologies like self-leveling, polyaspartic, and antimicrobial formulations improve functional performance, sustainability, and worker safety. Furthermore, regulatory compliance concerning environmental and workplace safety standards drives manufacturers to develop floor coatings with low volatile organic compound (VOC) emissions and enhanced durability against microbial growth and chemical exposure.

Asia-Pacific holds the largest market share in the industrial floor coating sector, fueled by aggressive industrialization, infrastructure development, and government initiatives promoting manufacturing hubs. Countries including China, India, and Vietnam are key contributors to this growth due to their rapidly expanding industrial base and industrial construction activity.

North America is the fastest-growing regional market. Growth here is supported by the expansion of advanced manufacturing facilities and strict regulatory requirements related to occupational safety and environmental sustainability. Increasing investments in the refurbishment of aging industrial infrastructure, as well as demand from sectors like aerospace, automotive, and food processing, are driving the adoption of high-performance coatings such as epoxy and polyurethane.

Europe shows steady market growth, largely due to stringent environmental regulations and a rising focus on eco-friendly, water-based, and solvent-free coating options. The expansion of the pharmaceutical and food industries within the region further supports demand for hygienic and durable floor coatings.

Epoxy-based floor coatings dominate the market due to their superior chemical resistance, durability, and strong bonding to concrete surfaces. They are highly favored in environments requiring resistance to heavy mechanical stress, including manufacturing plants, warehouses, and automotive facilities. Epoxy coatings also provide seamless, easy-to-maintain surfaces that contribute to operational efficiency and worker safety.

Polyurethane and polyaspartic coatings are also gaining popularity for their rapid curing times, flexibility, and high resistance to abrasion and chemicals. Water-based coatings are increasingly adopted for their eco-friendly profiles and compliance with environmental norms, particularly in sensitive sectors such as food processing and pharmaceuticals.

End-use sectors driving the market include manufacturing, food processing, automotive, aviation, and transportation. Manufacturing facilities represent the largest user base due to their expansive floor areas and requirements for durable, low-maintenance surfaces. The food processing sector is noted as one of the fastest-growing end-use segments, driven by regulatory requisites for hygienic and antimicrobial coatings.

Despite strong demand and technological advances, the industrial floor coating market faces challenges such as high initial installation costs and the requirement for skilled labor to achieve proper application. Complex application processes and downtime during installation may limit adoption in cost-sensitive markets. Nonetheless, these hurdles encourage innovation in installation techniques and formulation improvements aimed at reducing cost and complexity.

Emerging economies, particularly in Asia-Pacific and the Middle East, present substantial growth opportunities due to new industrial developments and infrastructure investments. Manufacturers focusing on eco-friendly and smart coatings, combining durability with environmental compliance, are well-positioned to capture market share.

The global industrial floor coating market is set for steady and sustained growth, underpinned by ongoing industrial expansion and a strong focus on safety and sustainability. Advanced coating technologies that enhance worker protection, floor longevity, and environmental responsibility will continue to be critical differentiators. Market players are increasingly dedicating resources to research and development, aiming to innovate with antimicrobial, anti-slip, heat-resistant, and low-VOC products.

In summary, the industrial floor coating market reflects the broader industrial trend toward smarter, safer, and more sustainable operational environments. With expanding demand across multiple regions and sectors, it offers significant prospects for manufacturers and end-users engaged in improving industrial infrastructure quality and workers’ safety.